News

Online Feature: Green H2 in Indian refineries—Challenges and opportunities

S. K. KASHYAP, HPCL, Visakhapatnam, India; and S. N. SHESHACHALA and S. SRIRAM, HPCL, Bengaluru, India

The UN Climate Change Conference (COP26) held last year in Glasgow, Scotland stressed the need for an immediate reduction in global greenhouse gas (GHG) emissions to preserve a livable climate. For many, COP26 signifies a last chance to combat the climate crisis before it is too late—countries reaffirmed the Paris Agreement goal of limiting the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit it to 1.5°C. Participating countries also stressed the urgency of action “in this critical decade” when carbon dioxide (CO2) emissions must be reduced by 45% to reach net-zero by 2050.

A provision was agreed upon calling for a phase-down of coal power and a phase-out of “inefficient” fossil fuel (oil and gas) subsidies. The Glasgow conference reaffirmed the pledge and urged developed countries to fully deliver on the $100-B goal. The Glasgow Pact called for a doubling of investment to support developing countries in adapting to the impacts of climate change and building resilience. The countries agreed to strengthen a network—known as the Santiago Network—that connects vulnerable countries with providers of technical assistance, knowledge and resources to address climate risks.

Throughout the COP26 conference, many significant agreements and announcements were made, including: 137 countries took a landmark step forward by committing to halt and reverse forest loss and land degradation by 2030; 103 countries, including 15 major emitters, signed the Global Methane Pledge, which aims to limit methane (CH4) emissions by 30% by 2030, compared to 2020 levels; more than 30 countries and six major vehicle manufacturers set out their determination for all new car and van sales to be zero-emissions vehicles by 2040 globally and 2035 in leading markets; and private financial institutions and central banks announced moves to realign trillions of dollars towards achieving global net-zero emissions.

Net-zero targets. Several countries have enacted laws or have policy documents made or announced their net-zero target or are in the proposal stage. According to the “Net-zero Tracker” of the Energy and Climate Intelligence Unit, 14 countries have enacted laws for net-zero targets, 33 countries have policy documents in place, 19 countries have announced their net-zero targets and 57 countries have proposals for net-zero targets. These commitments by countries are a testimony to the potential climate crisis envisaged by the countries in near future, if unattended.

During COP26, Indian Prime Minister Shri Narendra Modi committed India to a net-zero carbon emissions target by 2070. As part of the net-zero strategy, he presented “panchamrit” (five elixirs) or goals that would help the country to achieve its target for net-zero emissions by 2070. These are:

- India will take its non-fossil energy capacity to 500 GW by 2030.

- India will meet 50% of its energy requirements from renewable energy by 2030.

- India will reduce the total projected carbon emissions by 1 B metric t (tons) from now until 2030.

- By 2030, India will reduce the carbon intensity of its economy by more than 45% (from 2005 level).

- By the year 2070, India will achieve the target of net-zero.

Actions to achieve net-zero targets. The Ministry of Petroleum and Natural Gas, Government of India (MoPNG), has set up an Energy Transition Advisory Committee, which is tasked to prepare a step-by-step plan for the complete transitioning from fossil fuels to clean energy to achieve the net-zero emissions target by 2070. The Ministry of Power, Government of India, released its Green Hydrogen Policy in January 2022.

The Ministry of New and Renewable Energy, Government of India, is in the process of finalizing its “National Green Hydrogen Mission” document, the objective of which is to make India a global hub for green H2 production, usage and export. The mission is expected to lead to significant decarbonization of the economy, reduce dependence on fossil fuel imports, and enable India to assume technology and market leadership in green H2.

One specific objective of the mission is to progressively replace grey H2 with green H2 in petroleum refining and fertilizer industries from now to 2030–2035, with a gradual increase of green H2 percentage of the total H2 consumption by these industries.

The Indian petroleum industry and the H2 requirement. Indian petroleum refineries presently have a total of 1.4 MM metric tpy of H2 production from the steam methane reforming (SMR) process. This production is expected to reach 2.6 MM metric tpy by 2030 due to the addition of new facilities and hydroprocessing units. In addition to SMR, continuous catalytic reforming (CCR) is a significant producer of H2 as a byproduct. In some refineries, H2 recovery units are capturing H2 from H2-rich fuel gas and offgas generated from hydroprocessing units. These H2 recovery units are based on pressure swing adsorption (PSA).

Considering that H2 production from CCR and recovery from PSA are minor contributors to overall H2 production, the requirement of new SMR in India is significant (i.e., 1.2 MM metric tpy from now to 2030). This is 86% higher than the current installed SMR capacity.

SMR based on natural gas or naphtha is a major contributor to CO2 in the petroleum refining industry. One kg of H2 production can emit 8 kg–10 kg of CO2. Consequently, H2 production from naphtha or natural gas is the first target for decarbonization in refineries. The technological options for decarbonization of H2 production are blue H2 and green H2.

For Indian petroleum refineries, blue H2 has its own perceived challenges, including technologies for CO2 capture, space constraints for retrofitting within existing SMR units, high CAPEX and OPEX costs for a CO2 capture section, CO2 pipelines and transportation, and the availability of a dry well near refineries for sequestration or the availability of wells in the vicinity for enhanced oil recovery (EOR), among others. A CO2 capture section requires significantly higher power consumption. It is also believed that any additional power requirement for the carbon capture, storage and utilization (CCUS) section must be fulfilled from a green source; otherwise, it may not truly reduce CO2 from the overall H2 production. Considering this, blue H2 lacks the “buzz” in Indian refineries.

Green H2 production can be accomplished through the installation of water electrolyzers. This is independent of existing SMR and produces zero CO2 emissions. Power for water electrolyzers must be sourced from renewable power, and India is poised in an advantageous position with solar energy due to its geographical location. In the near future, renewable power is expected to be significantly cheaper than power produced from a thermal power plant. Considering this, the adoption of green H2 is comparatively easier in Indian refineries than blue H2.

Biomass gasification, another method of producing green H2, is not considered for bulk hydrogen production due to several challenges related to the aggregation of biomass, higher CAPEX, the maturity of the overall process, etc. The transition of Indian refineries from grey H2 to green H2 presents several challenges as well as opportunities, which are discussed in the following section.

CHALLENGES/OPPORTUNITIES FOR GREEN H2 IN INDIAN REFINERIES

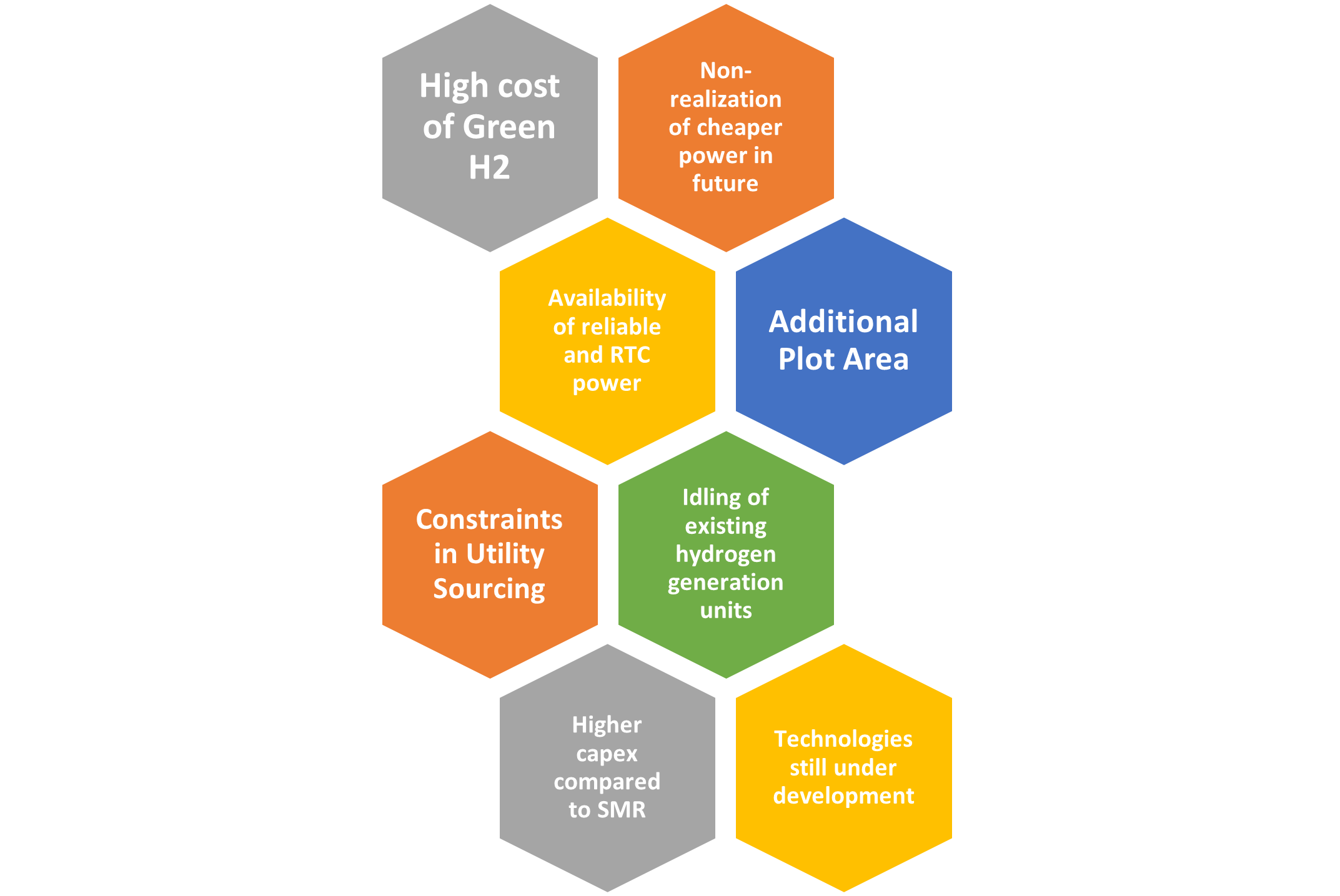

The introduction of green H2 in Indian refineries poses several challenges (discussed in detail below and shown in (FIG. 1), including:

- Higher production cost of green H2 compared to grey H2

- Possibility of non-realization of benefit of future low renewable energy cost

- Around-the-clock availability of reliable power

- Additional plot area requirement

- Constraints in utility sourcing

- Idling of existing grey H2 asset

- Higher CAPEX requirement compared to SMR

- Several water electrolyzer technologies remain under development.

Higher production cost of green H2 as compared to grey H2. In India (at the time of writing), green H2 costs an estimated $4/kg–$6.5/kg, and grey H2 costs around $1.6/kg–$2.2/kg. Considering a 10% replacement of grey H2 with green H2, Indian refineries must incur an additional cost of $377 MM/yr at present H2 consumption. This cost will further increase to $695 MM/yr by 2030 due to the increase in H2 consumption. In green H2 production, 77%–90% of the operating cost is attributable to green power, while the balance pertains to other utilities, such as feed water, repair and maintenance, cyclical cost of cell stack replacement, etc. Any reduction in green H2 cost will require a reduction in green power cost—other costs may not make a significant impact.

Possibility of non-realization of benefit of future low renewable energy cost. For any new green H2 facility, an agreement with a renewable power provider must be established for sourcing the required green power. Most renewable power providers require refineries (user) to agree to a long-term supply of power—some can be as high as 20 yr–25 yr.

Renewable power providers usually ask for a fixed power tariff for the complete duration of the contract due to the upfront CAPEX for installing the power infrastructure to match current requirements.

Going forward, renewable power cost is expected to fall for new installations due to economy of scale, improved technologies, an increasingly efficient supply chain and experience gained by the providers. However, the benefits of these measures and the coinciding lower power tariff will not be available for current green H2 facilities. Because of this, the cost of green H2 for current installations is not expected to decrease during their complete lifecycle.

At present, renewable power is estimated to cost Rs. 4/kW–Rs. 5.5/kW. In the future, this is estimated to drop gradually, depending on the maturity of the sector.

Around-the-clock availability of reliable power. India has four primary types of renewable energy installed: hydro, wind, solar and bio. As of Jan 2022, the total renewable energy installation in India [hydro (34%), wind (33%), solar (26%) and bio (7%)] stands at 152 GW, which is 38.6% of the overall installed power in India.

India’s government is targeting about 450 GW of renewable energy capacity by 2030. Of this, 280 GW (~60%) is targeted to come from solar and 120 GW (25%) from wind. The 50 GW–70 GW balance is expected to come from hydropower and others. Solar and wind are the two prominent renewable energy being considered in India for installation.

Renewable energy poses certain challenges with its around-the-clock availability. Due to the variabilities of renewable energy, a sustained power supply to industrial users is a challenge. According to one study, the country’s capacity utilization factor (CUF) of solar photovoltaic ranges from 15%–23%, depending on each location’s average radiation and ambient conditions. Most locations have a CUF of 18%. This means that power actually generated from the plant will be only 18% of the installed plant capacity. One of the major limiting factors is the limited availability of solar radiation during the daytime, typically 11 a.m.–4 p.m.

Similarly, wind power generation is dependent on wind speeds, which are dependent on climatic patterns. Normally, the monsoon season is considered a peak period for wind power generation in India. Seven states in the southern and western parts of India contribute ~95% of India’s wind energy. This concentration is primarily due to their geographical locations, where a large number of healthy wind days are experienced throughout the year. In 2020, wind energy generation in India was 24% lower in June, July, August and September compared to the same months in 2019. The primary cause for this reduction was lower regional wind speeds.

To overcome the variability of renewable energy sources, energy storage systems such as pumped hydro storage (PSP) systems and battery energy storage (BES) systems are being considered. A PSP system has multiple benefits, such as higher ramping capability, the capacity to smoothen fluctuations in renewable energy generation, support for frequency and voltage deviations in the grid, etc. A BES system presents several challenges, such as a shorter lifespan; higher capital cost; the requirement for expensive material such as lithium, nickel, cobalt, etc. Although PSP systems are being gradually adopted in India, the requirement is huge—India now has only ~3.3 GW of PSP systems under operation.

Due to the variability of renewable energy resources and the non-availability of adequate energy storage systems, around-the-clock power availability remains a challenge for sustained green H2 production at industrial scale.

Additional plot area requirement. Over the years, most Indian refineries have undergone several expansions in terms of crude capacity, fuel quality improvements, etc. Many refineries have further capacity expansion plans to meet the growing need for fuels. Additionally, Indian refineries are also considering diversification of their business into petrochemicals and specialty chemicals for improved margins and sustenance over the long time. These projects have significantly occupied available plot areas within refineries.

The installation of water electrolyzers at mega-scale capacity requires a significantly larger plot area, a challenge for already plot-constrained refineries. Considering 10% green H2 out of a total H2 requirement, Indian refineries must install ~1,100 MW of water electrolyzer plants now; this number will increase to 2,000 MW by 2030 due to the increase in H2 consumption. A 100-MW water electrolyzer plant is estimated to require a plot area of ~20,000 m2, including auxiliary facilities.

As H2 is a colorless, odorless and highly flammable gas, the installation of a water electrolyzer plant too far from a refinery and pipeline transportation may be infeasible for safety and economic reasons. For safe operation, it is essential to locate the plant either within the refinery or in close proximity. This will reduce H2 compression and transportation costs, and the plant can be operated in sync with hydroprocessing units with convenient coordination among crews. The plot plan availability for a green H2 plant within a refinery may pose challenges and/or limit other expansion or value-added project plans.

Constraints in utility sourcing. Water electrolyzers require various utilities, such as feed water, cooling water, instrument air, nitrogen, etc. For example, a 100-MW plant requires an estimated 20 m3/hr–28 m3/hr of feed water—the requirements of other utilities depend on the water electrolyzer technology selected. Water is a scarce utility and many refineries in India are operating with very limited water availability; some facilities have faced potential/partial shutdown due to water scarcity. The additional water requirements for green H2 production put additional stress on already water-constrained refineries. Coastal refineries can consider a seawater desalination plant for availing feed water; however, this is at a higher cost, resulting in higher green H2 cost. Land-locked refineries will experience challenges with water availability to supply water electrolyzers.

Idling of existing grey H2 asset. Indian refineries have already invested in SMR to meet their current H2 requirement. Considering a percentage of green H2 in the overall H2 requirement will leave the existing H2 asset partially underutilized. To compensate for the loss on return on investment (ROI) for the idle capacity of the asset, refiners must find an alternate mechanism to utilize the idle asset. Considering 10% green H2 in the total H2 requirement, 140,000 metric tpy of SMR capacity will be idle at present.

Refiners can utilize an idle asset to:

- Meet future H2 requirement for any expansion or new hydroprocessing unit in case the green H2 percentage in the overall H2 requirement does not increase significantly in the future. This case will be an unlikely scenario, considering net-zero targets of individual refiners and the country as a whole.

- Produce other chemicals from syngas and diversify the product portfolio. The idle capacity of an SMR can be utilized to produce of methanol, ammonia, etc. Refiners must make separate techno-economic analyses for these products. Government assistance in policies and viability gap funding will be required to make these projects attractive for refiners.

Higher CAPEX requirement compared to SMR. For future capacity expansion and hydroprocessing unit requirements, refiners essentially must consider green H2. Water electrolyzers are significantly more costly than SMR plants with the same capacity. For 50,000 metric tpy of H2 production, SMR is expected to cost $110 MM, whereas the same capacity of a water electrolyzer is expected to cost $440 MM. Although the cost of water electrolyzers is expected to reduce significantly in the future due to economy of scale, this comparison will need careful observation in future. Increasing commodity prices and the higher demand of water electrolyzer systems due to significant energy transition measures being considered by various organizations are causing some apprehension. The higher capital requirement for a green H2 facility will put financial stress on refiners unless support from the government is availed.

Several water electrolyzer technologies remain under development. Four main types of water electrolyzer technologies are available for green H2 production: alkaline, proton exchange membrane (PEM), solid oxide, and anion exchange membrane (AEM). Of these, alkaline and PEM are industrialized and being installed for commercial use. Solid oxide and AEM are still under development and are yet to be deployed at an industrial level.

While alkaline is the oldest technology for H2 production, it presents several challenges, such as larger plot area, lower current density, lower operating pressure, lower purity, corrosion, susceptibility to power fluctuation, etc. However, this is presently the most widely used technology and has a lower CAPEX requirement compared to other technologies.

PEM is an emerging technology and is being considered at a lower scale (i.e., 2 MW–10 MW). It has several benefits over alkaline technology in terms of plot area, current density, operating pressure, H2 purity, etc. However, it is not yet competitive with alkaline technology if compared over the complete life of the water electrolyzer system.

Solid oxide has a high electric efficiency that equates to higher H2 production for the same amount of electricity consumed by other technologies. However, as solid oxide operates at very high temperature, its component materials are thermally challenged. It also has a complex fabrication process and higher cost.

AEM is viewed as an alternative to PEM technology, with a lower cost due to the use of steel in place of titanium. Solid oxide and AEM are viewed as more advanced technologies than alkaline and PEM; however, further development and adoption of these technologies at an industrial scale remains imminent.

For now, Indian refiners face a limited choice of alkaline and PEM technologies for green H2 production at mega scale to meet their significant requirements. These technologies carry deficiencies or require higher capital cost that must be overcome with better, more economical technologies.

Opportunities. While several challenges exist for green H2 in Indian refineries, there are several opportunities, as well. Green H2 will help decarbonize the refining industry—Indian refineries are already setting targets to reach net-zero much earlier than the country’s target of 2070. Activities in the direction of net-zero help abate the climate risk for shareholders without disrupting returns in the long term, as well as leverage an improved reputation for serving customers that are climate conscious.

Green H2 adoption by Indian refiners provides an opportunity to diversify their businesses towards fuel products that utilize green H2.

Among the potential uses for green H2 are the shipping and transportation industries, as well as the manufacturing industries, such as steel and chemicals, where it can be used as raw material and/or fuel. Realizing the potential for green H2 will provide Indian refiners with a “first mover” advantage. The experience gained will be of immense help in utilizing it for other industries.

Takeaway. Indian refiners are already in the process of net-zero announcements and framing strategies to achieve the same. Green H2 is one of the most important levers for refiners to achieve net-zero. While the adoption of green H2 by Indian refiners presents challenges that must be overcome—the higher cost of green H2, non-realization of benefits of low renewable energy cost in the future, around-the-clock renewable power availability, plot and utility constraints, the idling of existing H2 assets, and higher CAPEX requirements, among others—it also provides opportunities that include decarbonization of the sector, a first-mover advantage, and business diversification.

To kick-start and provide the impetus for the adoption of green H2 by refiners, governments must formulate suitable policy structuring and bridge the financial viability gap for at least the short term.H2T

SUDHIR K. KASHYAP is the Chief Manager-Commissioning, at Hindustan Petroleum Corp. Ltd. (HPCL), Visakhapatnam, India. He has more than 15 yr of experience in refinery project execution involving conceptualization and strategy, technology selection and evaluation, feasibility studies and project execution for refinery projects. Kashyap holds a BS degree in chemical engineering from BIT Sindri and a post-graduate degree in oil and gas management from UPES Dehradun.

N. SHESHACHALA is a General Manager, R&D, at HPCL’s Green R&D Center in Bengaluru, India. He has more than 30 yr of experience in operations, economics and production planning at HPCL’s Visakh Refinery, as well as corporate functions like crude procurement, refinery-wide optimization, R&D, process engineering, modeling and simulation. He earned a BS degree in chemical engineering from Bengaluru University. Sheshachala holds patents in the area of PSA and rotating packed beds for gas treating applications.

S. SRIRAM is Chief General Manager, Process Technology, at HPCL’s Green R&D Center in Bengaluru, India. He has more than 30 yr of experience in the refinery projects, process safety and environment, operations and process analysis and design divisions. Sriram holds a BS degree in chemical engineering from TKM College of Engineering, Kollam, Kerala, India.

From The Archives

Connect with H2Tech